The House committee on small business and entrepreneurship development has approved a substitute bill which provides for an alternative to the onerous ‘5-6’ loan scheme to help in the survival of micro, small and medium enterprises (MSMEs) through access to rational and affordable financing schemes.

The committee chaired by Rep. Peter Unabia (1st District, Misamis Oriental) approved the unnumbered substitute bill to House Bill 5158 or the proposed “Pondo sa Pagbabago at Pag-asenso” or P3 Act.

House Bill 5158 with its full title, “An Act Providing A Socialized Microfinancing Program for Micro Enterprises Thereby Promoting Entrepreneurship,” is authored by Unabia, Reps. Jocelyn Sy Limkaichong (1st District, Negros Oriental), Rodrigo A. Abellanosa (2nd District,Cebu City), Gil P. Acosta (3rd District, Palawan), Alexandria P. Gonzales (Lone District, Mandaluyong City), Marisol C. Panotes (2nd District, Camarines Norte), Carlito S. Marquez (Lone District, Aklan), Salvador B. Belaro Jr. (Party-list, Ang Edukasyon), Bernadette “BH” C. Herrera-Dy (Party-list, Bagong Henerasyon and Jose Antonio Sy-Alvarado (1st District, Bulacan).

Unabia said access to financing is a persistent challenge which most MSMEs experience.

“Start-up and existing enterprises can usually get capital by seeking loans from lending institutions, such as banks, cooperatives or micro-finance institutions (MFIs),” said Unabia.

While there are several financing and credit programs for MSMEs, Unabia said these enterprises find it difficult to avail of them because of high interest rates and voluminous documentary requirements, including the need for collaterals.

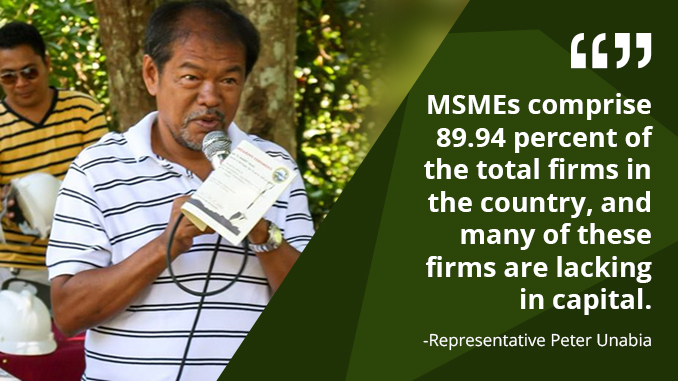

“MSMEs comprise 89.94 percent of the total firms in the country, and many of these firms are lacking in capital, and their survival in business relies heavily on access to financing. But instead of accessing traditional financing, micro enterprises resort to borrowing from the ‘5-6’ lenders,” said Unabia.

Under the bill, the P3 micro financing facility shall help micro enterprise owners optimize their potentials and achieve major growth through an alternative source of funding with a low interest rate.

A P3 Fund shall be created and lent out to qualified MSMEs under such terms and conditions that will meet the purpose of the said Act.

The beneficiaries of the P3 Fund shall be micro enterprises, entrepreneurs, including market vendors, agri-businessmen, members of cooperatives, industry associations and cooperators.

Rep. Angelina D.L. Tan, M. D. (4th District,Quezon), head of the technical working group (TWG) which crafted the substitute bill, said the measure will institutionalize the program which the Department of Trade and Industry (DTI) started to implement this year through the Small Business Corporation (SB Corp.).

“It aims to replace the ‘5-6’ money lending scheme and make available a micro lending facility with an interest rate lower than the prevailing market rate,” Tan said.

Tan said the TWG, in fine tuning the provisions of the bill, considered the comments and recommendations of the concerned agencies such as the DTI, SB Corp., Bangko Sentral ng Pilipinas (BSP), Rural Bankers Association of the Philippines, and Chamber of Thrift Banks.

The bill declares the State shall develop policies, plans and programs and initiate means to encourage entrepreneurial activities, and to ease the constraints and challenges to MSMEs, particularly on access to financing.

The bill aims to provide an affordable, accessible and simple micro financing program for the country’s micro-enterprises, especially those in the poorest communities.

It also provides that the SB Corp., the financing arm of the DTI, shall be the lead implementing agency for the P3 Fund. The SB Corp. shall handle fund delivery to micro enterprises through the following modes: direct lending to micro enterprises; wholesale lending to conduits, such as micro finance institutions (MFIs); rural banks; and credit cooperatives, which shall lend the fund to micro enterprises and provide guarantees to loans granted by the banks to qualified P3 beneficiaries.

An amount of not more than 10 percent of the total loans disbursed shall be provided annually to the SB Corp., to be sourced from the earnings of the P3 Fund to support the administrative and operating expenses of SB Corp.

The P3 Fund shall have the following features: Loan Fund; and Guarantee Fund of not more than 25 percent of the total loan exposure among others.